Will the Ukraine War Raise Inflation?

Will Putin’s invasion of Ukraine send inflation soaring past 10%?

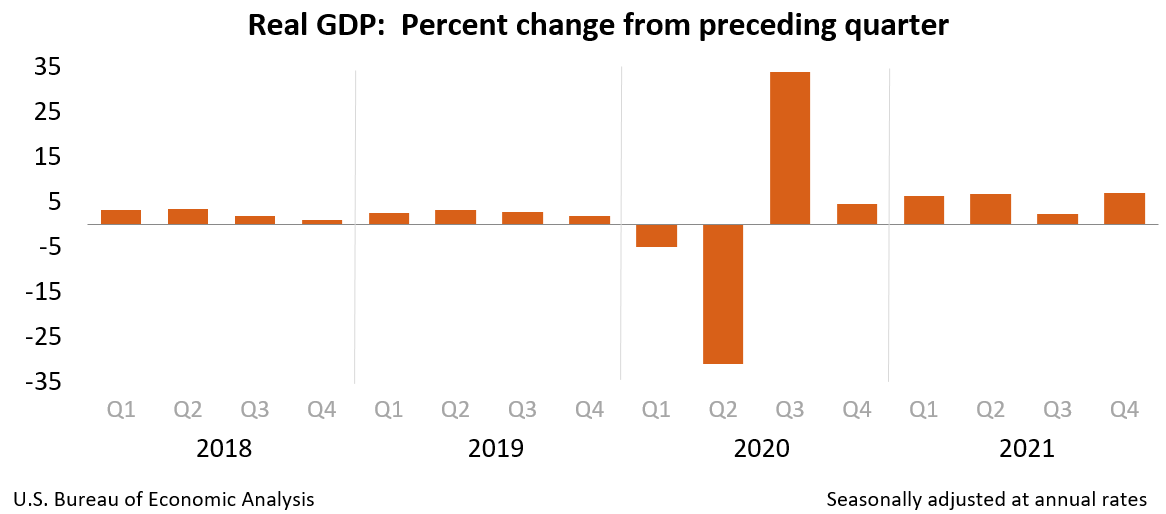

Before Ukraine, US inflation had already been soaring for a full year, indeed since Joe Biden took office. It was driven by excess spending, money printing, supply chains, paying people not to work, and regulations hitting everything from truckers to oil production. The White House especially was on full scapegoat mode, blaming everything from greedy meatpackers to online shopping to global warming, while mainstream media dutifully carried water; just last week CBS was widely ridiculed for trying to pin a year of soaring prices on Ukraine, which was invaded 3 days ago.

Still, in the first moments of Putin’s invasion, oil prices jumped for a moment, suggesting world oil markets are indeed interested in Putin’s more kinetic hobbies. So what comes next?

Whatever happens in Kyiv, the conflict will likely raise inflation even higher than today’s 7.5% annual pace. But the rise will probably be much less than feared, and certainly less than the world-is-ending permabears are warning. So higher inflation, but this probably isn’t the big one.

Why? There are 3 main mechanisms:

1. Cutting off the production and export of commodities, raising their price in global markets.

2. Rising economic risk, pushing central banks to stimulate the economy with yet more easy money.

3. Giving cover for central bankers to let inflation run, which they want to do but are currently afraid to.

Commodity Risk

First, cutting off commodities. While Ukraine produces plenty of sunflowers, the key commodity here is oil and natural gas. Ukraine doesn’t really produce either, but Russia does. So the concern isn’t Ukraine per se, it’s sanctions against Russia that freeze Russian exports.

How much oil are we talking? Russian production is about 11% of world output — about half the size of America’s 20%, but larger than Canada’s 6%. Russia’s share of oil exports are, also, around 11%. For natural gas, Russia is higher: about 18% of world production, but roughly 40% of gas imports to Europe.

So it’s a big producer, a big exporter, and it has enormous leverage over, above all, Europe.

So far this threat has been very muted, probably specifically because Europe is so addicted to Russian oil thanks to their self-crippling green policies. This makes Europe very much fear rocking the boat, hence world markets think Russian fossils will continue flowing.

Still, it’s possible that sanctions could raise the odds of a cut-off. Those sanctions, so far, are very targeted — Europeans don’t want any trouble. But there’s still a high chance of kicking Russian banks off SWIFT, the global payments system owned by major banks and overseen by central banks. Both Italy and Hungary just today endorsed kicking Russia off, having previously opposed, and it seems increasingly likely.

On the other hand, US banks also just today came out against a SWIFT exile. In fact, they explicitly fretted it “might encourage the development of a SWIFT alternative that could eventually damage the supremacy of the U.S. dollar.”

So the US, like Europe, has selfish reasons to forget the whole thing ever happened. More serious sanctions are still possible — cutting off Russia’s central bank is now being floated. But unless these come, the commodity cut-off scenario is unlikely.

Recession Risk

A second inflation mechanism is broader risk to the real economy. If disruption and shortages cause companies worldwide to pause investment or individuals to worry and save money. Both are on their own deflationary, but both usually spur central banks to stimulate even more to head off recession. This could mean central bankers keeping rates low for longer, or it could mean again ramping up their asset purchases (QE) and delaying sell-off of central bank assets (QT). All would pump inflation.

Like oil prices, so far this recession risk has been muted, at least going by equity markets: after a 2% plunge the day after invasion, the S&P soared 4% in the afternoon to end the day up 1.8%. It’s likely the rebound was so strong because sanctions were so limited, but the point is that the war itself doesn’t carry much inflation, it’s the sanctions that matter. Meaning that if serious sanctions don’t happen at all, the impact on the real economy, hence on inflation, will be pretty small.

Narrative Risk

Finally, the third and arguably most important mechanism: the narrative. Ukraine gives an excuse for central banks to pump the money-printer. Historically, central banks exist to push as much inflation as possible without voters turning on them. If shelled-out cities and rivers of refugees are filling the headlines, it’s a green-light for central bankers to get back to work debasing voters’ life savings. The American people will certainly grumble about higher prices, but if they blame Russia instead of the Fed then, from the Fed’s perspective, it’s costless.

This is even more likely because the Fed’s already worried about turning down the money printer, whether by raising rates, tapering off asset purchases (QE), or even selling off assets (QT). They’re nervous because last time they tried even a little tightening the markets panicked — the infamous “Taper Tantrum.” Meanwhile, even pre-Covid the money markets were doing things that keep bankers up at night. Any excuse to let it rip and not spook markets is welcome for a Fed that has painted itself into a very deep corner.

In sum, the real impacts to inflation -- commodity interruptions and economic risk -- will probably be limited unless sanctions get serious, in which case they could soar in the short-term. Either way, we’ll likely get higher inflation simply from giving cover to the Fed to keep the party going well past the guests falling over in comas.

How much will depend whether the American people buy mainstream media and White House spin that $6 gas or $5 lattes are Putin’s fault, or if they understand that inflation crises are, always and everywhere, caused by your own government and central bank.

What’s It Mean for Bitcoin?

Marginally higher inflation from central bankers with better excuses probably doesn’t have that much impact on bitcoin prices – your average Bitcoiner has probably already priced in 10% inflation coming down the pike.

On the other hand, world market sentiment does have a strong impact: that same crazy Thursday the S&P was bouncing down 2% then up 4%, Bitcoin was instead plunging 11% then rebounding 13%. So we can expect that kind of move again if markets repanic, but they won’t unless sanctions get much stronger. So both depend on sanctions.

Probably the most concrete long-run impact on Bitcoin is if Russia is kicked off SWIFT, which sends them in search of that alternative, whether some Russia-friendly clone or even Bitcoin. Moreover, a SWIFT exile raises the prospect that China could also be kicked off someday.

Given China’s share of cross-border payments, kicking miscreants off SWIFT could start to seriously erode the US dollar’s reserve currency prospects. We could then expect a crumbling dollar to encourage more countries to copy El Salvador’s magnificent Bitcoin reforms and get off the sinking ship while there’s still plenty of lifeboats.

In the end, whatever happens in Kyiv, we’ll likely see even higher inflation and even real erosion in the dollar's reserve status.

Thanks for reading, and subscribe for weekly updates. See you next time!